Cyprus entered the offshore natural gas industry in 2011 with the discovery of the Aphrodite field, approximately 160 kilometers south of Limassol. This finding marked a turning point for the small island nation, which had relied entirely on imported energy. The discovery sparked interest from major international energy companies and positioned Cyprus as a potential gas producer in the Eastern Mediterranean.

Since then, multiple fields have been discovered across Cyprus’s Exclusive Economic Zone, with reserves estimated at over 20 trillion cubic feet. However, transforming these underground discoveries into actual production has proven far more complex than initially expected, with technical challenges, political disputes, and commercial uncertainties creating substantial delays.

- The Journey From First Discovery to Development Plans

- Additional Discoveries Across Multiple Blocks

- The Path to First Production Through Egyptian Infrastructure

- Political Complications From Regional Disputes

- Regional Energy Security and European Connections

- Current Status and Future Outlook

- The Big Impact of Cyprus Gas Exploration

The Journey From First Discovery to Development Plans

American company Noble Energy received the rights to explore Block 12 in October 2008, well before any major discoveries in the region. The company suspected gas accumulations found in Israeli waters might extend northward. In September 2011, the Cyprus A-1 well confirmed these suspicions at the Aphrodite field. Follow-up drilling in 2013 with the A-2 appraisal well confirmed approximately 98 billion cubic meters of contingent resources with potential for an additional 26 billion cubic meters. The field sits in water depths of 1,700 meters and represents the first commercially viable gas discovery in Cypriot waters.

Noble Energy later sold stakes to British Gas, which was subsequently acquired by Shell in 2016. When Chevron purchased Noble Energy in 2020, it became the operator. Current partners include Chevron with 35 percent, Shell with 35 percent, and Israeli company NewMed Energy with 30 percent. Cyprus granted a 25-year production license in November 2019, but actual development has faced repeated setbacks. In September 2024, the partners submitted a revised development plan estimated at four billion dollars. The plan involves drilling four subsea wells connected to a floating production unit with capacity of 800 million cubic feet per day. Gas would be exported via pipeline to Egypt’s transmission system.

Cyprus approved this latest plan in February 2025, with partners committing to make a final investment decision in 2027. If approved, production might begin around 2027 at the earliest, though some observers consider 2031 more realistic. The long delay from discovery in 2011 to potential production reflects the commercial challenges facing offshore gas developments in small markets.

Additional Discoveries Across Multiple Blocks

Italian energy giant Eni and French company TotalEnergies discovered the Calypso field in Block 6 in February 2018, each holding 50 percent stakes. Initial estimates suggested reserves comparable to Egypt’s massive Zohr field, though subsequent analysis indicated more modest volumes. The partnership achieved further success in 2022 with discoveries at Cronos and Zeus, both in Block 6. Cronos holds an estimated 3.1 trillion cubic feet, while Zeus may contain 2.5 trillion cubic feet. These discoveries proved particularly significant because they lie near existing Egyptian infrastructure, offering potential for faster development.

ExxonMobil entered Cypriot waters in 2019 with its discovery of the Glaucus field in Block 10, operated jointly with Qatar Energy. Initial estimates suggested 5 to 8 trillion cubic feet, though later appraisal indicated approximately 3.7 trillion cubic feet. In July 2025, ExxonMobil announced the Pegasus discovery also in Block 10, featuring a 350-meter gas column. Combined reserves in Block 10, including Glaucus and Pegasus, might total 8 to 9 trillion cubic feet according to company officials. ExxonMobil plans appraisal drilling at Pegasus in 2027 before committing to development concepts.

The Path to First Production Through Egyptian Infrastructure

While Aphrodite receives most international attention as Cyprus’s first discovery, the Cronos field now appears likely to achieve production first. Eni has pursued an aggressive fast-track development strategy by leveraging its existing Zohr field infrastructure in Egyptian waters just 70 kilometers away. In February 2025, Egypt and Cyprus signed a host government agreement allowing Cronos gas to be processed at Zohr facilities and liquefied at Egypt’s Damietta LNG plant for export to European markets.

This arrangement offers substantial advantages. Cyprus possesses limited domestic gas demand, consuming less than one billion cubic meters annually. Any viable development requires export markets, but Cyprus lacks LNG facilities or pipeline connections to Europe. Egypt, by contrast, has existing liquefied natural gas plants with spare capacity. By connecting to Egyptian infrastructure, Cronos can reach production faster and at lower cost than standalone developments. Eni expects to finalize technical and commercial agreements in 2025, with first gas production targeted for 2027.

The Aphrodite partners are exploring similar arrangements. In February 2025, they signed a memorandum of understanding with Egypt for exporting Aphrodite gas through Egyptian transmission systems. However, the economics remain uncertain. Egypt pays relatively modest prices for pipeline gas compared to global LNG markets, reducing potential profits. Unless gas prices rise substantially or better commercial terms emerge, the project faces uncertain returns despite government approval.

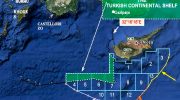

Political Complications From Regional Disputes

Cyprus’s gas exploration occurs in one of the world’s most politically contested regions. The island has been divided since 1974, when Turkey occupied the northern third following an Athens-backed coup. Turkey does not recognize Cyprus’s right to claim an Exclusive Economic Zone or license exploration blocks. Ankara argues that Turkish Cypriots possess equal rights to offshore resources and has asserted its own overlapping continental shelf claims in several areas.

These disputes have led to direct confrontations at sea. In February 2018, Turkish naval vessels physically blocked an Eni drill ship from reaching Block 3. Turkey has repeatedly sent its own drilling vessels into contested waters, escorted by warships. In 2019, Turkish operations off Cyprus’s southwestern coast prompted the European Union to impose limited sanctions, including suspended talks and reduced funding. However, these measures have not prevented continued Turkish exploration activities.

A separate dispute with Israel complicated Aphrodite’s development for years. Part of the reservoir extends into Israeli waters as the Yishai field. This cross-border situation required negotiations over revenue division. Israel and Cyprus agreed on a framework in March 2021, allowing companies to negotiate directly. This removed one obstacle, though commercial negotiations between operators required additional time before development could proceed.

Regional Energy Security and European Connections

The Eastern Mediterranean discoveries gained heightened significance following Russia’s invasion of Ukraine in February 2022. European countries desperately sought alternatives to Russian pipeline gas, making previously marginal projects more attractive. Cyprus’s proximity to Europe and connections to Egyptian LNG facilities offered potential diversification routes. Industry analysts suggested Cypriot gas could help reduce European dependence on Russian energy.

However, practical challenges remain substantial. The proposed EastMed pipeline connecting Israeli and Cypriot gas directly to Europe lost American backing in January 2022. The project’s estimated 6 to 7 billion dollar cost and technical complexity raised serious questions about economic viability. Any pipeline to Europe would need to cross waters claimed by Turkey, which explicitly opposes such projects unless Turkey receives benefits. Without Turkish cooperation, direct pipeline exports appear unlikely.

The global shift toward renewable energy also affects long-term prospects. Major energy companies increasingly prioritize renewable investments over fossil fuel projects. The global transition toward net-zero emissions means new gas infrastructure faces uncertain demand beyond the next two decades. Cyprus’s deep-water fields represent relatively high-cost developments that may struggle to compete in a future dominated by cheaper renewables.

Current Status and Future Outlook

As of early 2026, Cyprus stands at a critical juncture. Cronos represents the most advanced project, with final investment decision expected in 2025 and potential production by 2027. This timeline would make it the first Cypriot field to reach production despite being discovered years after Aphrodite. The Aphrodite partners moved forward with engineering design work in late 2024, though final investment remains uncertain pending commercial agreements with Egypt.

ExxonMobil continues evaluating its Block 10 discoveries. The company indicated that commercialization might occur between 2030 and 2035 if conditions align favorably. However, ExxonMobil has stated that large-scale LNG export projects would require significantly more reserves than currently confirmed. Cyprus Energy Minister George Papanastasiou regularly emphasizes the government’s desire for rapid development to reduce energy costs for Cypriot consumers.

The Big Impact of Cyprus Gas Exploration

Natural gas discoveries have fundamentally altered Cyprus’s strategic position in the Eastern Mediterranean. The findings transformed a resource-poor island into a potential energy exporter with regional leverage. The presence of global energy giants represents confidence in Cyprus’s future potential. These companies would not maintain operations and invest billions without believing in eventual profitability.

Yet the gas sector demonstrates that geological fortune alone cannot guarantee success. Cyprus possesses genuine hydrocarbon resources in commercially significant quantities. Converting those underground reserves into flowing production requires navigating technical complexity, volatile markets, infrastructure costs, and regional conflicts. After fifteen years of exploration and multiple discoveries, Cyprus still awaits its first commercial production. This timeline shows that modern resource development demands not just geological luck but also commercial viability, political stability, and patient capital willing to accept uncertain returns over extended periods.